Results review 4Q07

jsng@sbbsec.com.my

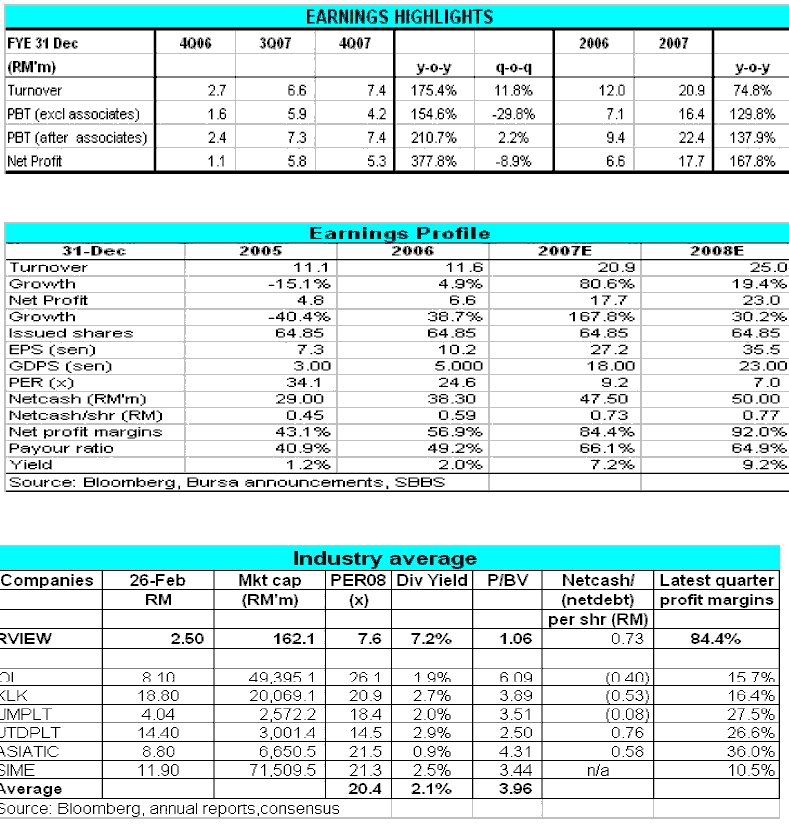

FY07 net earnings slightly below our forecast of RM19.8m. Riverview reported a solid FY07 results, as the topline and bottomline grew 80.6% and 167.8%, respectively, mainly due to higher average selling price realised for Fresh Fruit Bunch (“FFB”) on the back of buoyant CPO price (2007: RM2470/MT; 2006:RM1530/MT). Gains on disposal of quoted investments and increasing contributions from associates also contributed to the huge 137.9% jump PBT.

Q-Q, 4QFY07 turnover rose 11.8% to RM7.4m on the back of FFB’s higher average selling price amid skyrocketing CPO price (3Q07: RM2587/MT; 4Q07: 2888/MT). However, PBT before associates and net profit were down 29.8% and 8.9%, respectively mainly owing to: 1) lower operating income arising from forex losses of its RM17m deposits in foreign currencies such as sterling and AUS$ following the strengthening of Ringgit, 2) higher effective tax rates of 29.9% against 20.3% in 3Q07.

A stronger 2008 results anticipated. On the back of steady crop production of 12100MT coupled with the strengthening CPO price to RM3348 YTD from RM2470/MT in 4Q07, Riverview is envisaged to chalk up another strong 2008’s net earnings of RM23m (+xx% y-y), assuming steady FFB yields of 26tons/ha and average mature area at approximately 1,650-70ha due to its continuous replanting exercise.

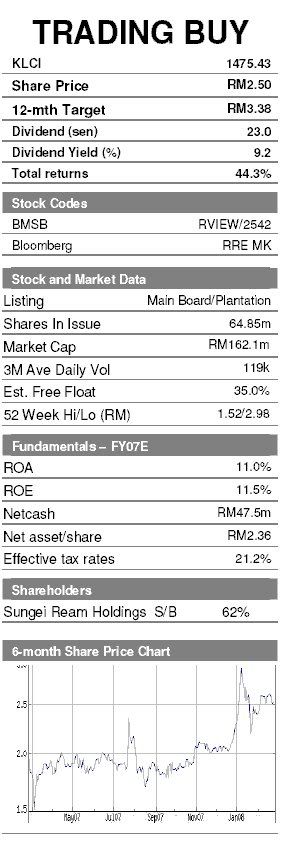

Higher dividend payout likely in future due to solid financials and limited capex for 2008. Riverview netcash stood at about RM48m in FY07. We believe that with its strong netcash inflow of average RM10m pa, Riverview cash pile will increase further in future in the absence of major acquisition and limited capex. Thus, we expect higher payout of 23sen (8.9% yield) from 18sen in FY07 and 5sen in FY06.

Bullish CPO outlook. We remain upbeat on CPO price prospects as supply deficits for other edible oils will encourage consumers to switch to palm oil, amid reports of weather setbacks in key oilseeds fields in South America, India and China, together with a revival in crude oil prices. On top of that, the fight for acreage between grains and oilseeds is set to intensify on the back of lower-than-expected wheat supply.

Wheat prices recently rallied to a new high following reports of potential losses of wheat crops in India and China as well as lowerthan- expected Canadian wheat stocks. In addition, some key crop producing countries have resorted to prohibitive tax on exports of vegetable oil to curb inflationary pressure at home. Indonesia for example recently announced that it would raise the export tax on CPO from 10% to 25% if international prices exceed US$1,100 per tonne.

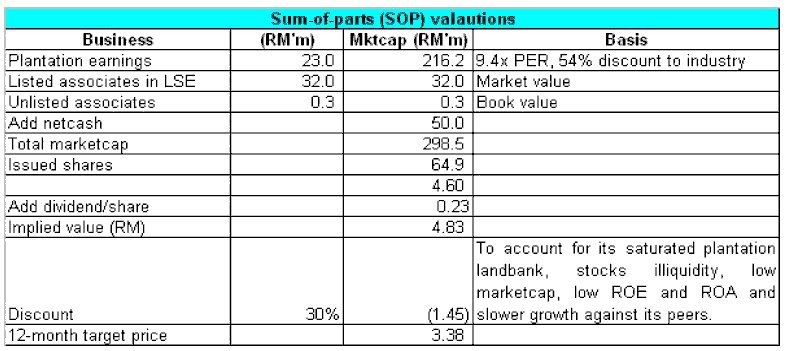

12-month target price at RM3.38/share. We value Riverview based on a sum-of-parts valuation method comprising: 1) a 9.6x PE valuation for the plantation business; 2) market value for its listed associate, book value for its unlisted associate and 3) estimated net cash per share as at end-2008. Our sum-of-parts value amounts to RM4.60. Adding a net dividend per share of 23sen estimated for 2008, we obtain our implied value of RM4.83. Nevertheless, we adopt a 30% discount to the value to compensate for the group’s the saturated plantation landbank, stocks illiquidity and market capitalization, as well as the prime yielding age that limiting the scope for future yield expansion despite offering superior margins, attractive yield, solid financials and good leverage to CPO prices. Thus, our 12-month target price still offers a 31% upside from current price at RM2.58.

Riverview4Q07.pdf

以上的average selling price应该是分析员附加的,并不是rview报价。

rview是少数的蚊型股,比sbagan小。

rview的大股东是Sungei Ream Holdings Sdn Bhd,他和sbagan没有关系。

这里不赘述sbagan了,他们根本风马牛不相及。

但如果你不知道sbagan,那么你就很难理解rview。

rview的盈利来自1800公顷棕油园,利息收入,和两家associate companies。

两家associate companies,一家在英国上市(在大马种植)。

利用sotp work out fair value是最好的方法了,但我不同意分析员定价英国股价,却只给malaysia associate RM300,000的估值。Narborough Plantations PLC今年的股东大会已经是第98届,另一家unlisted associate company-Rivaknar Holdings Sdn. Bhd.的资本近RM5,000,000。

Narborough也同时持有33.3%Rivaknar。

Narborough Plantations PLC的股价,处于合理水平。

只分享研究所得,非鼓励买卖。

No comments:

Post a Comment