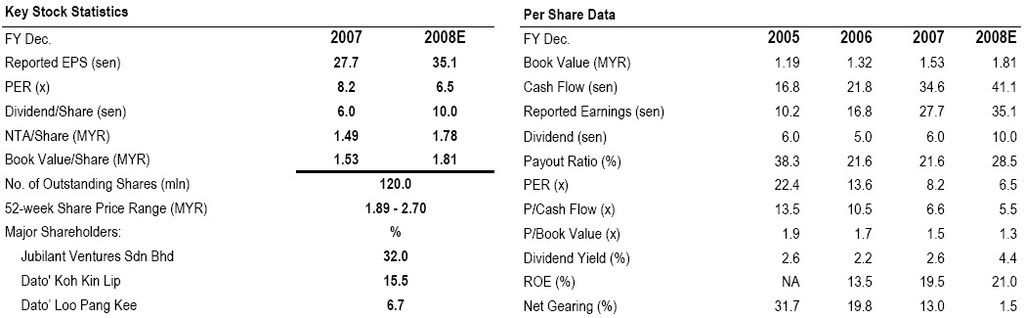

1.Sindora, HOLD , Price: MYR1.84

2.Sindora Berhad,net research,2QFY08 Result Update

3.NPC Resources,HOLD

4.Leweko Resources,HOLD

5.Kwantas Corporation Berhad,FY08 Results Within Expectations

6.Kwantas Corporation,BUY

7.Kulim,1HFY12/2008 Results

8.Kulim (Malaysia),September 3, 2008

9.Keck Seng (M),September 4, 2008

10.Keck Seng,2QFY08 RESULTS UPDATE

11.Boustead Holdings Berhad,Results Update

12.IOI CORPORATION,What’s next after Menara Citibank buy?

13.IOI Corporation Bhd,2 September 2008,No bargains in Citibank building

14.Plantations sector update, 5 September 2008

skip to end

1.Sindora, HOLD , Price: MYR1.84 back to top

12-Month Target Price: MYR2.10

Date: September 3, 2008

Analyst: Siti Rudziah Salikin

Market Value - Total: MYR176.6 mln

Summary: Sindora has two core businesses, namely: (i) oil palm and rubber plantations, and (ii) “Intrapreneur Venture” (IV) businesses, comprising entrepreneur-driven growth companies in various manufacturing and services sectors.

Results Review & Earnings Outlook

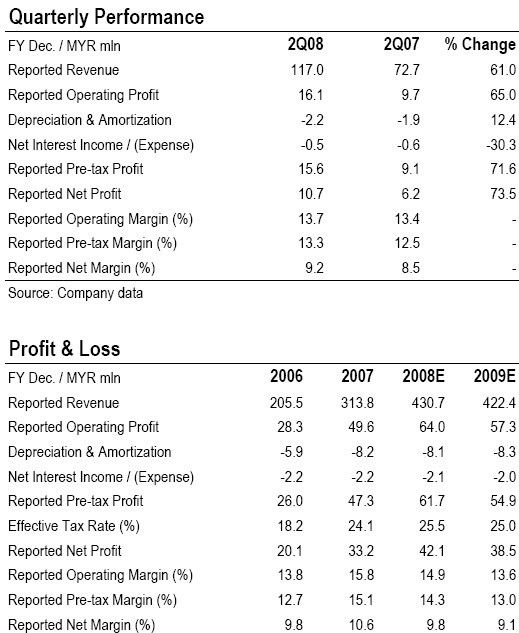

Sindora’s 2Q08 net profit doubled YoY to MYR6.7 mln but fell behind our expectations. FFB production declined 16% QoQ, due, we believe, to replanting. The decline was larger than expected. Overall, FFB output in Johor was lower sequentially in 2Q but the decline was small at 2.5%. The output was still higher YoY.

1H08 net profit was MYR18.1 mln, up 3.1x YoY, and accounted for 48.4% of our original full-year forecast. Plantations recovered from a weak period in 2007 with higher production and stronger selling prices. Sindora switched to selling on spot in late 2007, allowing it to capture a CPO selling price that was on par to the benchmark Malaysian Palm Oil Board average price of about MYR3,500/ton. Operating profit for the plantation operations jumped to MYR18.1 mln from MYR1.83 mln in 1H07.

Pre-tax contribution from the IV businesses was down 6.6% YoY to MYR10.3 mln, and was in line, as depreciation and interest expenses increased together with the expansion of the businesses.

In spite of the drop in price and its spot selling practice, we expect Sindora to be able to achieve an average CPO price of MYR3,000/ton in 3Q. Given our view that the price will recover from the current level in 4Q, we believe our projected CPO price of MYR3,200/ton for 2008 is within reach. However, we cut our net profit for 2008-2009 by 13% respectively, after lowering our estimated crop production for the two years.

Recommendation & Investment Risks

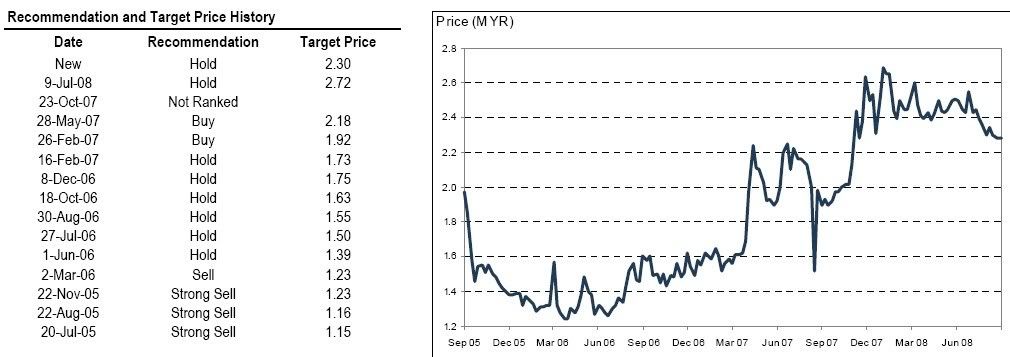

We downgrade our recommendation on Sindora to Hold (from Buy) with a lower 12-month target price of MYR2.10 (from MYR2.90).

Earnings are expected to peak in 2008 with net profit projected to decline 10.2% YoY in 2009 due to our assumption of lower palm oil prices. There is, however, potential upside to our forecast as we have not factored in E.A. Technique’s planned acquisitions of two more tankers later in 2008. We expect E.A. Technique, which is a shipping company that services major oil and gas companies, to lead the growth for the IV businesses. The concern would be Sindora’s rising borrowings to fund the expansion of the IV businesses.

We continue to use a PER to value the stock but have lowered our assigned multiple to 7x (from 8x) in line with the drop in peer valuations.

Risks to our recommendation and target price include an economic slowdown, which could impact the overall growth prospect of the IV businesses. The outlooks for the shipping business and plantation operations are also affected by the cyclical movement of crude oil and palm oil prices, in our opinion.

2.Sindora Berhad,net research,2QFY08 Result Update back to top

Lim Boon Ngee

4 September 2008

Price: RM1.84

HOLD

Sindora’s 2Q08 results were within our expectations. Revenue in 2Q08 increased by 25% yoy due to stronger plantations contributions on a 19.5% yoy increased in CPO production and higher average CPO price of RM3,545/tonne from an average of RM2,142/tonne in 2Q07. Revenue at the Intrapreneur Venture (IV) division, which accounted for 62% of total revenue, was flat yoy.

At the pre-tax and net profit levels, Sindora posted relatively stronger yoy increases of 57% and 39% respectively, due mainly to margin expansion at the plantations division.

We have lowered our PER-based RNAV estimate in line with the fall in market-wide valuations. At our revised RNAV estimate of RM2.00/share, Sindora’s implied FY09 PER is 5x, which we believe is deserved at this point given unexciting projected earnings growth in 2009. With limited upside to our price target, we are downgrading our recommendation to HOLD.

Revenue & Earnings

1H08 revenue increased by 36.5% yoy, reflecting higher CPO production and stronger average CPO prices. Revenue at the IV business was largely maintained yoy in 1H08.

Relative to revenue, profits at the pre-tax and net levels were sharply higher, due to a surge in plantations margins.

Balance Sheet

Sindora ended Jun 2008 with an estimated net gearing level of 76%, down from a net gearing level of 95% as at the end of 2007.

We expect Sindora’s gearing level to improve going forward, with cashflows from the plantations and in the absence of any major acquisitions. In addition, the group will be receiving sales proceeds from the disposal of its stake in MM Vitaoils for RM14.5m and the sale of a 20.5 acre piece of land to KFC Holdings for RM6.2m.

Dividends

No dividends were declared in 1H08.

Earnings Outlook

At the IV division, the group had on 15 Jul 2008 terminated the proposed acquisition of a 71.2% stake in JM Permata, a company involved in the trading of baby products, due to non-fulfilment of conditions precedent and breach. Sindora has also announced that it is disposing of its 35% stake in MM Vitaoils in 3Q08. We have adjusted our earnings estimates to reflect these two proposals.

2008 revenues and earnings are expected to continue to register double-digit growth rates based on our estimates, underpinned by a stronger plantations division and sustained growth at the IV division.

We are however projecting relatively flat growth in 2009, given our assumption of lower average CPO prices and in the absence of any new IV business acquisitions.

3. Recommendation

We have lowered our PER-based RNAV estimate in line with the fall in market-wide valuations.

At our revised RNAV estimate of RM2.00/share, Sindora’s implied FY09 PER is 5x, which we believe is deserved at this point given unexciting projected earnings growth in 2009. With limited upside to our price target, we are downgrading our recommendation to HOLD.

3.NPC Resources,HOLD back to top

Price: MYR2.28

12-Month Target Price: MYR2.30

Date: September 2, 2008

Market Value - Total: MYR273.6 mln

Summary: NPC Resources (NPC) is one of the smaller oil palm plantation groups in the country. NPC operates 8,774 hectares (ha) of oil palm plantations and two palm oil mills with a combined production capacity of 120 tons/hour in Sabah. NPC also owns the Berjaya Palace Hotel Kota Kinabalu and a fish rearing business.

Results Review & Earnings Outlook

NPC’s 1H08 results fell behind our expectations. While net profit grew 83.1% YoY to MYR20.7 mln, it only accounted for 36.8% of our fullyear forecast.

The growth in production (due to yield recovery and larger harvesting areas) and higher palm oil prices drove 1H08 revenue to MYR216.9 mln, up 16% YoY. Margins eased lower to 15.6% from 15.7% in 1H07, which was against our expectations and its peers’ performance. We had expected the higher palm oil prices to make up for the increased production costs arising primarily from higher fertilizer and fuel prices.

We cut our net profit forecast for 2008 and 2009 by 25.8% and 26.9% respectively after adjusting our cost assumptions. Looking forward, we expect seasonally stronger crop production in 2H to cushion the drop in selling prices.

The government has abolished the import duty on fertilizers effective Sep. 1, 2008. At this stage, we are uncertain whether the suppliers or importers will pass on the cost savings to planters. For 2008, we also understand most of the fertilizer requirements have been locked in early in the year. Therefore, we have not factored in the impact of the removal of import duty into our forecast.

Recommendation & Investment Risks

We maintain our Hold recommendation on NPC. 2008 PER of 6.5x is within the current valuation range of 5x-8x for small cap plantation stocks.

We revise our 12-month target price to MYR2.30 (from MYR2.72) following the downgrade in earnings and cash flow estimates. We use a discounted cash flow method to value NPC, assuming a long-term CPO price of MYR2,500/ton, and a WACC of between 8.7% and 9.8%.

We expect NPC to be in a net cash position in 2008 given the strong cash inflows from the plantation operations and relatively small capex needs. As such we project a higher dividend of 10 sen for 2008 (including the interim dividend of 6 sen per share), providing a decent yield of 4.4%.

4.Leweko Resources,HOLD back to top

Price: MYR0.38

12-Month Target Price: MYR0.49

Date: September 2, 2008

Market Value - Total: MYR43.7 mln

Summary: Leweko is an integrated timber group with upstream forest concessions and downstream manufacturing of sawn timber, moulded timber and other timber products. The group also owns 998 hectares of oil palm plantations. Analyst: Siti Rudziah Salikin

Results Review & Earnings Outlook

Leweko’s 2Q08 performance remained weak and was behind our expectations. Net profit for the quarter slid to MYR1.2 mln from MYR1.7 mln in 1Q08 and MYR4.8 mln in 2Q07. 1H08 net profit was MYR2.9 mln versus our full-year forecast of MYR6.5 mln.

The timber division was impacted by weak demand from Europe (Leweko’s main market), lower selling prices of timber molding products, and its full dependency on log supply from third parties. It recorded a loss of MYR2.2 mln in 1H08 compared with a profit of MYR9.6 mln in 1H07.

The plantation division disappointed us with a 27.4% QoQ drop in 2Q08 operating profit as higher palm oil prices were offset by lower FFB output and increased production costs. The profit was still higher YoY. Operating profit for 1H08 surged 2.2x YoY to MYR6.9 mln.

Leweko resumed third party log harvesting works in late June 2008, which should help to improve the timber division’s performance in 2H. However, the plantation division will feel the effect of lower palm oil prices in the 2H.

We cut our earnings forecast for the plantation division but after factoring in contributions from the log harvesting contract, we keep 2008 net profit unchanged at MYR6.5 mln and raise 2009 profit by 6.8% to MYR6.3 mln.

Recommendation & Investment Risks

We maintain our Hold recommendation on Leweko despite the recent share price correction, which increases the potential upside to the share price to 28.9%.

The prospects of demand recovery and earnings outlook for the downstream timber operations remain uncertain, which could drag the share price performance, in our opinion. The palm oil slide will also hamper the prospects of the plantation division, which is currently the earnings savior.

The target price is based on an unchanged 40% discount (to reflect the uncertain prospect of recovery) to our projected NTA for 2008.

Leweko is expanding into timber flooring production through its proposed acquisition of 51% stake in SCK Wooden Industries Sdn Bhd. We believe the acquisition, which is targeted for completion in 4Q08, will be accretive to Leweko’s earnings. However, the net impact (after factoring in the consolidation of SCK’s borrowings of MYR7.0 mln) could turn out to be small. We have not factored in the impact of the acquisition into our forecast.

Risks to our recommendation and target price include: (i) a prolonged downturn in the housing markets in Europe and the U.S., which will delay the recovery of demand for Leweko’s downstream timber products; and (ii) a continued downtrend in palm oil prices.

5.Kwantas Corporation Berhad,FY08 Results Within Expectations back to top

Tuesday, 02 September 2008

Analyst : James Ratnam (TA)

Share Price : RM2.85

Target Price : RM4.55

Market Capitalisation (RMmn) : 888.3

Recommendation : BUY

FY08 Results Within Expectations Kwantas reported a 94% YoY increase in FY08 earnings to RM150.7mn, well within our estimates. The improved earnings came on the back of 75.7% YoY increase in revenue to RM3.4bn, reduced interest cost as well as lower effective tax rate. Average CPO selling price increased 54.7% to RM2,831 per tonne. The downstream manufacturing business to benefited from higher selling prices and increased volume, particularly its shortening/margarine as well as refined soya bean oil produced at its plant in Guangzhou. Meanwhile, the biomass energy business posted lower operating profit of RM2.9mn (-17% YoY) due largely to 8.6% decline in revenue.

Modest Upstream Growth

Based on data made available in Bursa Malaysia, we estimate FFB production grew by approximately 3.4% YoY to 633k tonnes. We believe higher mature acreage is the main contributor to the increase in production. Up to 3Q08, the latest data made available to us, mature area has increased by 1,125 ha to 13,494 ha. CPO production meanwhile grew only by a marginal 1.5% to 130k tonnes.

China Manufacturing Business Growing Strong… The China downstream business recorded a sharp 45% increase in revenue YoY to RM851.7mn. as highlighted above, this was due to higher selling prices as well as volume. Management indicated demand is still strong despite the concern of slowdown in economy. The plants there too benefited from hedging of feedstock since last year, resulting in an exceptionally high profit margin in FY08. Nonetheless, this factor should normalise in FY09. On the contrary, we understand that the refining margin in the Malaysian operation has narrowed due to effect of rising feedstock cost.

But New Plants Commissioning Delay Could Cool Growth Ahead We understand that the commissioning of the 250 tonnes fatty acid production in Zhangjiagang had to be postponed due to the Olympics. The construction of the two soap noodle plants in Guangzhou and Zhangjiagang respectively too have been completed and currently undergoing testing, but yet to commence commercial operation. According to management, there is no indication yet from the authority on when the group could begin operation of the fatty acids plant. We feel the delay could well extend into 4Q of the calendar year or early next year.

Maintain Buy With Revised TP of RM4.55 We have trimmed FY09 and FY10 earnings forecasts by 7.2% and 4.5% respectively to take into account, 1) the delay in commissioning of the fatty acids and soap noodles plants, 2) lower profit margin assumption (4.2% vs. 4.4% previously) for the China manufacturing business as feedstock price likely to reflect the actual market price ahead, and 3) higher fertiliser cost.

Consequently, target price has been adjusted lower to RM4.55, based on 8.6x fair PER. The stock is trading at 5x forward PER despite the company's low sensitivity to CPO price, thanks to extensive exposure to downstream business, should mitigate earnings volatility. Kwantas remains a Buy.

6.Kwantas Corporation,BUY back to topKwantas Corporation,BUY

September 3, 2008

Analyst : Siti Rudziah Salikin

Share Price : RM2.88

Target Price : RM4.55

Market Capitalisation (RMmn) : MYR897.6 mln

Recommendation : BUY

Summary: Kwantas is a fully-integrated plantation group. It has 14,678 hectares (ha) of planted oil palms in Sabah and is developing another 33,848 ha of land in Sarawak. Its downstream manufacturing operations are located in Sabah and China.

Results Review & Earnings Outlook

Kwantas’ FY08 (June) results were 16% below our forecast at the pretax level but a lower tax rate reduced the discrepancy at the net level to 5.3%. Group pre-tax profit doubled to MYR212.1 mln while net profit rose 94% YoY to MYR150.7 mln.

The main discrepancies came from a slightly lower average CPO selling price of MYR2,831/ton (up 63% YoY) versus our forecast of MYR2,950/ton, and lower 4QFY08 revenue for its China operations.

Driving the growth was the surge in palm oil prices. CPO output was relatively flat at 132,324 tons. Revenue from China operations rose 44.9% YoY to MYR851.7 mln on increased sales of shortening/margarine products and seasonal trading of refined soya bean oil produced by its oils and fats processing facilities in Guangzhou.

In spite of the drop in palm prices, we expect Kwantas’ performance to be cushioned by its downstream activities. The concerns would be intense competition from the bigger players in China, which could put pressure on margins for Kwantas’ operations in the country.

We lower FY09 net profit by 12.2% after reducing our projected revenue from China operations in view of a continued delay in the commencement of the soap noodle, oleochemical and glycerine plants. We also introduce our FY10 net profit of MYR148.6 mln.

Recommendation & Investment Risks

We maintain our Buy recommendation as we believe the weaker-thanexpected results have been factored into the share price.

We continue to like Kwantas for its management efficiency, fullyintegrated operations (which will cushion the downside earnings risks from a weakness in palm oil prices) and decent dividend yields.

Nonetheless, we lower our 12-month target price to MYR3.30 (from MYR4.45, previously). The target price is based on 7x PER on projected FY09 earnings. The assigned PER has been reduced from 8x previously due to lower peer valuations.

Kwantas also has a sizeable reserve which could potentially be distributed to shareholders in the form of a bonus issue, in our opinion. This could help improve share liquidity.

Risks to our recommendation and target price include: (i) continued CPO price volatility, which could affect the performance of the plantation and manufacturing divisions; and (ii) an economic slowdown in China.

7.Kulim,1HFY12/2008 Results back to topKulim,1HFY12/2008 Results

inter-pacific research

2 Sept 2008

OUTPERFORM

Current Price: RM 7.60

Target Price: RM13.10

Results Highlights:

Improved performance, but fell below expectations: Though revenue for 1HFY12/2008 accounted for 57.4% of our full year forecast, net profit in 1HFY12/2008 only reached 42.9% of our full year forecast. This is mainly due to lower margins achieved in the plantation division. For 1HFY12/2008, revenue increased by 60.7% y-o-y to RM1,997.1 million whereas PBT rose 153.1% to RM411.5 million. The significant earnings were mainly attributed to higher CPO selling prices and turnaround of Malaysia plantations after a difficult year in 2007. However, on a q-o-q basis, though revenue rose 34.1%, PBT fell 6.6% due to lower margins which we believe were contributed by higher fertilizer and fuel costs. PBT margin for this quarter was at 17.4% as compared to 24.9% in 2QFY12/2007.

Lower margins from plantation: Plantation division achieved revenue of RM469 million for this quarter which is an increase of 22.7% q-o-q but EBIT fell 26.3% q-o-q to RM129 million. On a closer look, EBIT from Malaysia plantation dipped by 53.8% q-o-q to RM24.6 million whereas PNG & SI plantation EBIT fell at a lesser degree by 14.3% to RM104 million.

Improved performance across other segments: Oleochemical business has done exceptionally well this quarter as revenue and EBIT rose by 39.2% q-o-q and 137.7% q-o-q respectively to RM456.8 million and RM53.1 million respectively. QSR performance also improved moderately with revenue increasing by 1.8% q-o-q to RM131.2 million, thus lifting EBIT by 6.1% q-o-q to RM27.6 million.

Lower CPO prices to affect earnings: Going forward, we expect Kulim’s earnings to be affected by lower CPO prices. We are assuming CPO prices to average at RM2,500/MT for 2nd half of this year and RM3,000/MT for CY2009, thus we are lowering our earnings forecast by 27% for FY12/2008 and 12% for FY12/2009 to factor in lower CPO prices and higher production costs.

Recommendation & Valuation

OUTPERFORM: We remain optimistic on Kulim’s prospects despite bearish news of rising CPO supply, expected demand rationing due to global economic slowdown and downtrend of crude oil prices as we believe edible oil supply will remain tight attributed to demand growth from emerging markets, expected increase in biodiesel production due to lower edible oil prices coupled with increasing supply risks of edible oils and crude oil amid rising geopolitical tensions and weather woes. Besides, Kulim’s fast food and oleochemical businesses will continue to lend support to its earnings which will somehow mitigate the volatility in CPO prices. Another boost to Kulim’s earnings would be the commencement of its biodiesel plant in Oct 2008 as the lower CPO prices trading at a discount of RM400/MT to crude oil prices have made biodiesel production commercially viable again. We reiterate OUTPERFORM with fair value of RM13.10 based on sum-of-parts valuation. We believe this company remains one of the cheapest entry to oil palm industry as it is still trading at a mere 5.7x PER based on FY12/2009 EPS of RM1.33.

8.Kulim (Malaysia),September 3, 2008 back to top

Price: MYR7.50

HOLD

12-Month Target Price: MYR8.50

Market Value - Total: MYR2,259.1 mln

Analyst: Siti Rudziah Salikin

Summary: Kulim is an integrated palm oil producer, with oil palm plantations in Malaysia, Papua New Guinea (PNG) and the Solomon Islands. It also one of the world’s largest oleochemical producers and is the controlling shareholder of KFC and Pizza Hut restaurants in Malaysia, Singapore and Brunei.

Results Review & Earnings Outlook

Kulim recorded a 2.3x YoY growth in net profit for 2Q08 to MYR89.9 mln but the performance was below our expectations. 1H08 net profit rose 2.5x YoY to MYR188.1 mln and accounted for 44.6% of our original full-year forecast.

Palm oil selling prices for its Malaysian operations were lower than expected. Its average CPO selling price in 1H08 was up 41.5% YoY to MYR2,787/ton but remained at a large discount to the industry’s average price of about MYR3,500/ton. We had expected the gap to narrow to about 10% given its revised forward selling practices. In PNG and the Solomon Islands, the performance was affected by late shipment of about 18,000 tons of palm oils, deferring about USD9.0 mln in profit. Plantation operations in Malaysia contributed MYR77.9 mln or 18.9% to group pre-tax profit while the operations in PNG and the Solomon Islands contributed MYR231.0 mln or 56.1%.

Pre-tax profit contribution from the non-plantation segment grew 35.1% YoY to MYR107.6 mln with better performance from both the oleochemical operations and the QSR (QSR MK, MYR2.45, Hold) group as well as a two-month consolidation of Sindora’s (SDRA MK, MYR1.84, Hold) results.

We lower our projected net profit for 2008 by 17.7% and for 2009 by 17.0%, after cutting our average CPO price assumptions and factoring in the recent earnings downgrade for Sindora.

Recommendation & Investment Risks

We downgrade our recommendation to Hold (from Strong Buy) with a lower 12-month target price of MYR8.50 (from MYR12.00) following an earnings revision and a fine-tuning of our valuation parameters.

We believe the downside risk to Kulim’s earnings in 2H08 is higher. In Malaysia (and Indonesia), the drop in palm oil price will be partly cushioned by seasonally stronger production in the 2H. The operations in PNG and the Solomon Islands will not have this support as production typically peaks in the 1H of the year. At this stage, the only reprieve is the delayed recognition of the USD9 mln profit to 3Q.

The target price is derived from PER-based sum-of-parts method. We continue to value of each division at a discount to forward multiples of its peers but have lowered our assigned PERs by between 10%-15% due to the drop in its peer’s valuation. Implied 2008 PER at our target price is 7.0x, which is within the range of valuation of plantation-based companies in Malaysia.

Risks to our recommendation and target price include: (i) a prolonged weakness in CPO price which could be due to the volatility of mineral oil prices; and (ii) political instability in PNG.

9.Keck Seng (M),September 4, 2008 back to top

Price: MYR4.00

HOLD

12-Month Target Price: MYR4.90

Market Value - Total: MYR958.0 mln

Analyst: Siti Rudziah Salikin

Summary: Keck Seng (M)’s primary businesses include: (i) oil palm cultivation, (ii) refinery operations, (iii) hotel and resort management, (iv) property development and management, and (v) share investments. The group has been listed on Bursa Malaysia Securities since 1977.

Results Review & Earnings Outlook

Keck Seng’s 1H08 results were above our expectations with net profit of MYR56 mln accounting for 65.3% of our original full-year forecast. The profit was 53.3% higher YoY driven by increased sales volume of refined oils and higher selling prices of palm oil.

The surprise came from a margin improvement for the manufacturing division despite the higher feedstock costs. The division contributed MYR17.9 mln, up 4.9x YoY, or 21.9% to group pre-tax profit.

Plantations gained from the increase in palm oil prices and posted a 2.2x YoY rise in pre-tax profit to MYR12.8 mln. Profit for property development rose 16.9% YoY to MYR16.9 mln while that for hotel operations increased 8.4% YoY to MYR15.1 mln.

We are looking at lower earnings in 2H due to a drop in palm oil prices and high material costs. After adjusting for the better-than-expected margins for the manufacturing division, we raise our 2008 net profit forecast by 8.1% to MYR92.6 mln and by 7.7% to MYR90.4 mln for 2009.

Recommendation & Investment Risks

We maintain our Hold call on Keck Seng with a lower 12-month target price of MYR4.90 (from MYR5.20).

We continue to value the stock at a 30% discount to our projected NTA for 2008 of MYR4.72 per share. The discount is within the range of what we have applied to other small- to mid-sized property developers domestically. Implied 2008 PER (at 0.7x NTA or intrinsic value of MYR3.30) is 8.5x, which is also within the range of multiples for small cap plantation stocks.

We add the present marked-to-market surplus value of its investments of MYR1.58/share (down from MYR1.89/share) to the intrinsic value to arrive at the target price. We refrain from being more aggressive in our call on the stock despite the potential 22.5% upside to the share price, given that about a third of Keck Seng’s valuation comes from the surplus value of its investment, which carries downside risks with the current equity market volatility.

Risks to our recommendation and target price include: (i) a consolidation in CPO prices, which would affect the group’s plantation earnings, (ii) poorer-than-expected consumer sentiment which would affect the take-up of its properties in Johor, and (iii) continued volatility in capital markets which would impact the value of its equity investments.

10.Keck Seng,2QFY08 RESULTS UPDATE back to top

29 August 2008

ZJ Research

Price : RM4.06

Market Capitalisation : RM980.1m

Recommendation : BUY

1. 2QFY08 Results – exceed expectations

Keck Seng posted another strong quarter with 2QFY08 revenue and net profit increased 58.3% yoy and 15.7% yoy to RM407.8m and RM34.4m respectively. 1H08 net profit of RM56.0m accounted for 73% of our full year projection of RM76.5m.

1HFY08 revenue soared 59.6% yoy to RM736.3m on the back of improvements across all business segments. The best performing segments are plantations and manufacturing (comprising palm oil mill, refinery plant and production of palm and laurics products) which saw revenue up 87.6% yoy and 80.7% yoy to RM22.0m and RM592.9m respectively. The remarkable performance from these two divisions was largely due to the run-up in CPO price, which averaged at RM3,500/tonne in 1HFY08 vs. RM2,200/tonne in 1HFY07 (+59% yoy). Meanwhile, revenue from the property development division revenue rose 24.7% yoy, property investment (+4.6% yoy), hotels and resorts (+5.7% yoy) and share investments (+43.5% yoy).

Corresponding to the strong revenue growth, operating profit in 1HFY08 too was up 58.5% yoy to RM83.3m, while net profit surged 52.5% yoy to RM56.0m.

Keck Seng continues to be in net cash position, with net cash per share of 75 sen compared to 54 sen in 1QFY08. NTA/share stood at RM4.68 as at June 2008.

Keck Seng declared an interim dividend of 4.5sen less tax for the quarter under review.

2. Recommendation

With the strong 1HFY08 performance, we are revising our FY08 net profit projection upward by 11% to RM85.2m from RM76.5m. Our revised forecast however, assumes that 2HFY08 results would be weaker than that of 1HFY08, premised upon 1) the recent steep decline in crude palm oil price affecting the group’s plantations and manufacturing divisions; and 2) the current high inflations are likely to dampen its property division’s prospect. We note that the crude palm oil price has fallen from a high of RM4,300/tonne in March 2008 to the current level of circa RM2,500/tonne.

We are maintaining Buy call on Keck Seng but have decided to lower our fair value from RM5.45 to RM5.14 to account for the weaker market sentiments. Our fair value is derived based on a blend of adjusted NTA/share and a lower PER multiple of 13x (previously 15x). Although 2HFY08 performance may be subdued, the group’s fundamentals are intact and we remain positive on Keck Seng’s outlook in the longer term.

11.Boustead Holdings Berhad,Results Update back to top

Wednesday, 20 August 2008

Analyst : James Ratnam (TA)

Price : RM4.80

Target Price : RM6.22

Market Capitalisation : RM3,019.4m

Recommendation : BUY

1H08 Earnings up 99%

Boustead delivered another strong quarter of earnings growth. 2Q08 net profit rose 69.8% YoY to RM151.9mn on the back of 82% increase in revenue, although on QoQ comparison, net profit was lower due to decline in FFB output and increase in harvesting cost. 1Q08 net profit rose to RM304.2mn, a 99.1% increase YoY and accounts for 58% of our FY estimate.

Better Performance from Key Business Divisions

Both plantation and property division performed better compared with last year although bulk of the higher profit was due to consolidation of earnings from the heavy industries. The heavy industries accounted for 64% of the increase in 1H08 pretax profit.

Plantation division benefited from both, higher selling prices (+52.8% to RM3,314 per tonne) and to a lesser extent, increase in FFB production (+1.3% YoY), partially offset by lower harvest mature of 11% due to disposal of the Indonesian land bank. The property division profits meanwhile rebounded strongly in 2Q08 due to sale of two corporate lots as well as higher income from its property investments, particularly Royale Bintang hotels and The Curve.

Lucrative Margin from OPV Contracts

Management has always been tightlipped about the profit margin of the OPV contracts. The heavy industries division reported RM202.4mn operating profit on RM680.5mn revenue, which translates into 29.7% operating margin. Excluding the contribution from BHIC, we estimate margin from the OPV contracts could be in the region of 30%, higher than our initial 15% - 20% estimate.

Upgrade in Earnings Forecasts

We have revised downward average CPO selling price to RM2,900 per tonne (RM3,300 per tonne previously) given the weak price trend 2H08 to-date. FY09 selling price assumption remains unchanged at RM3,200 per tonne as we expect price to recover in 4Q or early next year. Concurrently, we have adjusted upward margin assumption for the OPV contracts to 30% from 20% before. The net impact is a 4.3% - 9.5% upgrade in FY08 - FY10 earnings forecasts.

RM7.10 Revised TP. Boustead is an Attractive Buy

We have rolled over the valuation base year to FY09. We have also cut the fair target PER of the heavy industries division to 9x from 12x before due to the sharp de-rating of the regional oil & gas sector, which is only trading around 8x currently.

Consequently, target price has been adjusted lower to RM6.22. Nonetheless, the stock has corrected significantly and even after the target price revision, potential capital appreciation is close to 30% and therefore, Boustead remains a buy.

12.IOI CORPORATION,What’s next after Menara Citibank buy? back to top

2 September 2008

HOLD

RM5.10

Target Price: RM4.30

Rationale for report : Company update

Gan Huey Ling

YE to June FY07 FY08 FY09F FY10F

FD EPS 22.7 35.0 34.0 34.7

FD PE (x) 22.5 14.6 15.0 14.7

IOI Corporation Bhd (IOI) announced that it would be acquiring Menara Citibank via Inverfin Sdn Bhd, for RM586.7mil. IOI will also assume borrowings of RM160.3mil.

Therefore, the effective purchase consideration for Menara Citibank is RM747mil, which translates into a net acquisition price of RM1,018/sq ft based on net lettable area of 733,626 sq ft. The acquisition is expected to be completed in 4Q2008.

Rental revenue of Menara Citibank amounted to RM43.3mil in FY07, which works out to be RM4.92/sq ft. Based on this, we estimate the cap rate for Menara Citibank at 4.6%. Menara Citibank currently enjoys a 99% occupancy rate.

We are neutral on the acquisition of Menara Citibank. Earnings contribution from Menara Citibank is not expected to be significant, increasing IOI’s FY09F net profit by less than 1%. Inverfin Sdn Bhd, which owned Menara Citibank recorded a net profit of RM20.4mil in FY07.

IOI is not expected to face any problems financing the acquisition as the group has gross cash of RM1.3bil as at end-FY08. Although the group issued a US$600mil exchangeable bond issue last year, IOI has only used proceeds of US$348mil. This means that IOI still has unutilised proceeds of US$252mil or RM822mil.

In the longer-term, we wonder if IOI would sell the property to its subsidiary, IOI Properties as the asset is a better strategic fit for IOI Properties. We also wonder if IOI would venture to buy another office building in the future.

We maintain a HOLD on IOI due to uncertainties in the price outlook of crude palm oil resulting from a supply imbalance situation and softening crude oil prices.

13.IOI Corporation Bhd,2 September 2008,No bargains in Citibank building back to top

UNDERPERFORM Maintained

RM5.10 Target: RM4.60

Mkt.Cap: RM31,325m/US$9,228m

The news

Buying Menara Citibank. IOI Corp has entered into an agreement to buy 100% of Inverfin Sdn Bhd from Menara Citi Holding Company (50%), CapitaLand (30%) and Amsteel Corporation (20%) for RM586.7m cash. Inverfin owns and operates Menara Citibank.

Details of the building. Menara Citibank is a 50-storey office building with five levels of basement car parks shared with Nikko Hotel. It is situated in the heart of Kuala Lumpur’s Golden Triangle and is 500 meters from the Petronas Twin Towers in KLCC. It has a net lettable area of 68,156 sq m (733,626 sq ft), which can be increased to 70,492 sq m (758,769 sq ft). The building currently enjoys a 99% occupancy rate.

Gross acquisition value of RM733.6m. The gross acquisition value for Menara Citibank, including the company’s net debt, is RM733.6m. As such, the gross acquisition price works out to be RM1,000 psf of the present net lettable area. In FY12/07, the building fetched gross rental revenue of RM43.3m, excluding RM3.3m revenue from the car park. This works out to an average gross rental rate of around RM4.90 psf per month and a gross rental yield of 5.9%. In FY07, Inverfin reported a net income of RM20.4m on revenue of RM46.7m.

Cash reserves to fund acquisition. IOI Corp will finance the purchase with its cash reserves. On top of that, it will advance Inverfin the amount necessary to repurchase the RM160m nominal amount of medium-term notes (MTN) 2007/2014 issued on 30 August 2007.

Rationale for the acquisition. The group sees the acquisition as a strategic move that gives it the golden opportunity to own one of the few available high-rise Grade A office buildings in Kuala Lumpur with a first-class location. The deal is expected to be completed in 4Q08.

Comments

Not a surprise. We are not surprised by this news as IOI Corp earlier revealed to the market that it had succeeded in its bid for Menara Citibank and would make an announcement after signing a definitive agreement with the vendors. This is a fairly major acquisition for the group as the gross purchase price of R733.6m makes up 8.7% of the group’s shareholders funds as at 30 June 2008.

Negative on the acquisition. Although the gross purchase price is 8.3% below the speculated price tag of RM800m, we take a negative view for the following reasons: (1) The RM1,000 psf pricing is at peak market prices. While the pricing is reasonable given the RM950-1,200 psf pricing for newer buildings under construction in the vicinity, bear in mind that Menara Citibank is more than 10 years old. (2) The location is good but not great, being on the fringe of the KLCC area and near other old buildings such as Menara OSK and Ampang Park. Furthermore, it does not have an unobstructed view of the KLCC park. (3) Tenant concentration risk is high as Citibank, the largest tenant, occupies 42.7% of the total lettable space and the building’s top five tenants take up 69.6% of the total net lettable area. (4) Menara Citibank currently enjoys one of the highest rental rates for Grade A office space in prime locations for new tenants at RM7.20 psf/month probably because of its blue-chip tenant, Citibank. If Citibank moves out, the yield may fall as other buildings nearby do not command such high rents. (5) Another negative point is that Menara Citibank recorded historical gross rental yield of 6% and net rental yield of 3.1%. This is below most prime office buildings, which give a gross rental yield of 7-8%. For many REITS, the gross yield is double digit and net yield is 8-10%.

The acquisition also appears to be a diversification from the group’s core businesses of plantation and property development. Also, IOI Corp’s current property investment portfolio comprises buildings mostly built by the group’s own property projects.

Earnings-neutral acquisition. This acquisition will not break the bank as IOI Corp has RM2.9bn cash and continues to derive strong cash flows from its core businesses. But net gearing will go up from 37% to 42%. However, the 2.7% net profit return from the asset is broadly in line with the 3% return on cash balances. As such, we expect the acquisition to have a neutral impact on earnings.

Valuation and recommendation

Maintain UNDERPERFORM. We are keeping to our earnings forecasts as the acquisition is expected to be earnings neutral. Overall, we are negative on the deal as we are of the opinion that the acquisition of the prime office building does not put the group’s funds to good use. They should instead buy plantation estate as the returns are better in the long run and that is the main core expertise of the group. Although we are negative on the deal, we are leaving our target price at RM4.60, based on an unchanged forward P/E of 13x as the acquisition will have minimal impact on earnings and the acquisition price is fair. Retain UNDERPERFORM rating, with the key derating catalysts being the softening CPO price, weaker property market and rising operating costs.

14.Plantations sector update, 5 September 2008 back to top

UNDERWEIGHT Maintained

Key takeaways from POTS2008

POTS conference overview

2nd International Palm oil Trade Fair & Seminar. We recently attended the 2ND International Palm Oil Trade Fair & Seminar 2008 (POTS 2008) themed “Changing Marketing Landscape – Challenges for Business Sustainability”. The event was organised by the Malaysian Palm Oil Council (MPOC) and drew some 400 participants from around the world.

Issues discussed. A total of 16 speakers with various backgrounds spoke on issues relating to three key themes: (1) policies and regulations influencing the oils & fats dynamics; (2) market fundamentals and price outlook and (3) environmental sustainability and international competitiveness. On top of that, there were two plenary lectures entitled “Targeting opportunities & managing challenges in the commodities market” and “Why palm needs biofuel demand for its long-term success?”. We summarise below the highlights from the conference.

Key takeaways

Bearish CPO price predictions. Only two speakers touched on the CPO price outlook. Mr Dorab Mistry, a well-known and regular speaker on the conference circuit since 1996, has turned bearish on CPO price prospects, ditching his May 08 forecast of a CPO price of RM4,500 by Feb 09. This is due to demand destruction for major edible oils due to the high prices since 1Q08, ideal weather conditions since mid-June for all major planting areas so far and expectation that the high cycle of palm production will stretch to Oct or Nov instead of the earlier projection of Sep. Overall, he estimates supply of edible oils to exceed demand by 1.45m tonnes for Sept/Oct 08 and 0.3m tonnes for 2009. As such, he feels that the correction in CPO price over the past two months is justified. He also thinks that palm oil price needs to be cheaper than fossil fuel to attract strong demand and clear the excess supply. Overall, he believes that the market may be slightly oversold and could see a recovery. In the short term, he sees strong support for CPO price at RM2,200 if crude oil price stabilises at US$100 per barrel. He refrained from making a CPO price forecast for 2009 and will probably reveal it at the next conference in Singapore on 11 Sep and in Mumbai on 28 Sep. However, it is not all doom and gloom for CPO price given the growing uncertainty surrounding US crops and the possibility of an earlier-thanexpected end to the monsoon in India. This could disrupt crop supplies and boost price prospects. Mr Abdul Rasheed, CEO and Director of Mapak Edible Oils predicted that CPO price for the remainder of the year will be RM2,400-2,700 per tonne if crude oil price is US$100-110 per barrel and RM2,700-3,000 per tonne if crude oil is US$120-130 per barrel.

Policies and regulations impacting palm oil trade. We gathered from the conference that Pakistan’s government has accorded a 10% discount to the import duty for palm oil from Malaysia under the free trade agreement (FTA). This has enabled Malaysia to raise its share of palm oil imports to Pakistan over the past two years (see Figure 1). Mr Mistry also warned that India may consider raising import duties on palm oil when inflationary pressures ease. Another new regulation to watch out for is REACH, a chemical legislation in Europe which will affect the way manufacturers, importers, formulators and end users conduct business in Europe and globally. It is estimated that this new legislation could add €2.8bn-5.2bn to the industry over 11 years. This will affect oleochemical and certain biodiesel producers that export their products in Europe. A speaker also spoke on the issues and challenges in meeting the RSPO certification as well as the high costs involved in qualifying for the certification. The additional costs involved include certification fees, maintenance costs, environment conservation and preservation costs and costs to address social issues (internal as well as external at the estates). It was revealed that all these could add up to as much as 10% of the current operating costs for estates.

Oleochemical industry prospects. Mr Cheah Seng Chye who is attached to IOI Oleochemicals spoke on the changes and challenges in the oleochemical market. In his paper, he forecast that the supply of the two main oleochemical products, fatty alcohol and fatty acids, will exceed demand in 2009. Apart from overcapacity, other challenges faced by the industry include (1) securing of future feedstock given the limited land available for new plantations; (2) new legislation like RSPO and REACH which could boost the operating costs of oleochemical products, (3) shortage of cargo space; and (4) increasing freight rate.

Comments

CPO price expectations lowered. We are not surprised that conference speakers have pruned their CPO price expectations. This is because global edible oil supply has improved since then and demand has been dented by the high prices. On top of that, the sharp decline in mineral oil price has the effect of lowering the floor price for CPO and the recovering US$ has caused funds to flow out of commodity-related products, which were previously seen as a hedge against inflation. All these concerns are not new and were highlighted in our earlier plantation updates. The key surprise was the price forecast of as low as RM2,200 per tonne for CPO in the near term should crude oil price decline to US$100 per barrel. We are generally less bearish than the speakers and expect a stronger 4Q price due partly to our more bullish inhouse crude oil assumption and expectation of slower palm oil supply growth from Malaysia due to seasonality.

Challenging times for planters. Overall, the conference gave us a better awareness of the challenging market environment that palm oil producers and manufactures face over the next few years. What surprised us during the conference was the high cost of getting Roundtable on Sustainable Palm Oil (RSPO) certification, equivalent to as much as 10% of the total operating costs of estates. This fact is not well-known to the market as most planters are in the process of obtaining the certification on a stage-bystage basis. Unless consumers are willing to pay premium pricing for certified CPO, the certification costs could add to the operating cost pressure on planters, which are already hit by the rising fertiliser, petrol and labour costs. It remains unclear at this juncture if the certified palm oil could command a premium over the uncertified CPO to help cover the certification cost. If not, the process could raise the cost of producing CPO, making the crop less cost competitive than other edible oil crops.

Valuation and recommendation

Downside to our CPO price forecast. There is downside risk to our CPO price forecast for 2008 as our expectation of a RM3,200 average for 2H08 appears to be a tall order now given the high palm oil inventories, subdued demand and weakening crude oil price. Assuming that CPO price stays at around the current level, there is RM200 downside risk to our 2008 price forecast of RM3,350 per tonne. Our 2009 forecast of RM3,000 remains achievable as weather uncertainty weighs on US crop prospects.

Maintain UNDERWEIGHT call. The main takeaways from the conference are the cost risks for planters who are pursuing RSPO and the downside risk to RM2,200 per tonne for CPO price. We retain our UNDERWEIGHT call on the plantation sector in view of the challenging earnings prospects stemming from weaker selling prices and rising operating costs. Our top pick for exposure to the sector is Sime Darby for its high dividend yield and M&A potential. Key de-rating catalysts for the sector are weaker CPO price, improvement in the weather prospects for key planting areas, lower mineral oil prices and a stronger US dollar.

end of bulk upload back to top

No comments:

Post a Comment